1. What is the Oil Country Tubular Goods Market Overview – definition, scope, and significance?

The Oil Country Tubular Goods (OCTG) market comprises steel pipes and tubing used in drilling, completing, and producing oil and gas wells. It includes seamless and welded pipe variants, and product categories such as drill pipe, well casing, and production tubing. These tubulars are essential for maintaining well integrity, handling high pressures, and ensuring safe extraction of hydrocarbons both onshore and offshore. The market’s significance lies in its direct impact on exploration efficiency, cost control, and overall energy supply security.

2. What are the main drivers, restraints, challenges, and opportunities shaping the Oil Country Tubular Goods Market?

Key drivers include rising global oil demand, increased upstream investment, and the expansion of offshore projects that require high‑specification tubing. Technological advances in drilling (e.g., extended‑reach and ultra‑deepwater wells) boost demand for premium OCTG. Restraints involve volatile oil prices, which can delay capital expenditures, and strict environmental regulations that pressure operators to adopt alternative energy sources. Challenges stem from supply chain disruptions and the high cost of raw steel. Opportunities arise from the growth of unconventional resources, digital monitoring of pipe performance, and emerging markets investing in new exploration activities.

3. What are the current growth trends in the Oil Country Tubular Goods Market?

Current trends show a shift toward seamless pipes for high‑pressure applications, driven by offshore deepwater projects. Welded tubing is gaining traction in onshore fields where cost efficiency is paramount. Manufacturers are investing in advanced metallurgical processes to improve corrosion resistance and tensile strength. Additionally, the market is witnessing consolidation, with major steel producers acquiring niche tubing firms to broaden product portfolios and enhance global reach.

4. How has COVID‑19 impacted the Oil Country Tubular Goods Market and what is the recovery trajectory?

The pandemic caused a temporary dip in demand as drilling activities were suspended worldwide during 2020. Supply chain bottlenecks and reduced capital spending further compressed volumes. Recovery began in late 2021 as oil prices rebounded and operators resumed drilling. By 2023, demand had recovered to pre‑pandemic levels, and the market is now on a steady growth path supported by renewed upstream investment.

5. Who are the major competitors and what is the level of consolidation in the Oil Country Tubular Goods Market?

Leading competitors include ArcelorMittal SA, JFE Steel Corp, Nippon Steel Corp, Tenaris SA, Vallourec SA, and TMK Group, among others. The market is moderately consolidated, with a few large steel manufacturers holding significant share, complemented by specialized tubing companies such as Jacob Tubing L.P. and Kelly Pipe Co. Recent mergers and strategic alliances have further concentrated market power, enabling economies of scale and broader product coverage.

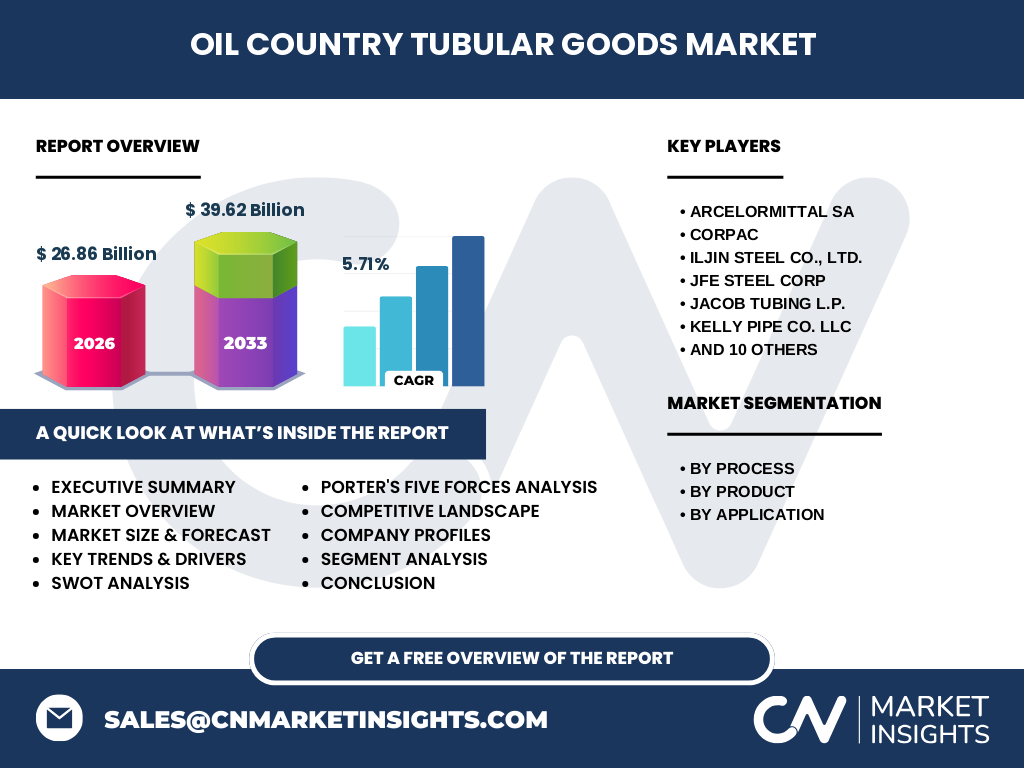

6. What are the key findings in the executive summary of the Oil Country Tubular Goods Market?

The OCTG market is valued at $26.86 billion in 2026 and is projected to reach $39.62 billion by 2033, reflecting a CAGR of 5.71 %. Seamless pipes dominate high‑pressure segments, while welded products grow in cost‑sensitive onshore projects. Regional demand is driven by offshore expansions in the Middle East and increasing onshore activity in North America. Competitive pressures are intensifying through consolidation, and technological innovation remains a primary growth lever.

7. What are the forecast expectations for the Oil Country Tubular Goods Market from 2025 to 2032?

Based on the provided CAGR of 5.71 %, the market is expected to continue expanding steadily. By 2032, the market size is anticipated to approach the upper end of the forecast range, maintaining momentum from offshore deepwater developments and the resurgence of onshore unconventional drilling. Investment in advanced steel grades and digital monitoring solutions will further sustain growth.

8. How is the Oil Country Tubular Goods Market sized and shared by segmentation?

Segmentation by process divides the market into seamless and welded categories. Seamless tubes command a premium due to superior strength, especially for offshore and high‑pressure wells, while welded tubes attract cost‑conscious onshore projects. By product, drill pipe, well casing, and production tubing each serve distinct phases of well construction; drill pipe sees the highest turnover during drilling phases, whereas well casing and production tubing dominate during completion and production stages. Application segmentation separates onshore and offshore demand, with offshore driving higher‑grade seamless products.

9. What is the global distribution of Oil Country Tubular Goods Market size and share by region?

The market exhibits a balanced global footprint. North America remains a major consumer due to extensive shale activity, while the Middle East and North Africa lead offshore demand. Asia‑Pacific shows rapid growth fueled by new exploration projects in China and India. Europe maintains a stable share, largely focused on maintaining existing infrastructure. Each region contributes proportionally to the overall market size, aligning with regional drilling activity levels.

10. What are the key performance highlights in the regional analysis of the Oil Country Tubular Goods Market?

North America’s growth is driven by unconventional shale plays, leading to steady demand for welded tubing and production tubing. The Middle East’s offshore expansion fuels seamless pipe usage, especially for deepwater projects. Asia‑Pacific’s emerging basins generate both seamless and welded demand, with China’s domestic production increasing self‑sufficiency. Europe’s market is characterized by maintenance and replacement cycles, sustaining modest but consistent demand across all product types.

11. Which companies lead the Oil Country Tubular Goods Market and what are their strategic approaches?

ArcelorMittal SA focuses on high‑performance seamless tubes and global distribution networks. Tenaris SA leverages a broad product portfolio and strong service capabilities. Vallourec SA emphasizes innovation in corrosion‑resistant alloys. TMK Group pursues vertical integration and capacity expansion. Smaller players such as Jacob Tubing L.P. and Kelly Pipe Co. concentrate on niche markets and customized solutions. Strategic moves include capacity upgrades, joint ventures, and digital service platforms to enhance customer engagement.

12. How does Porter’s Five Forces model assess the Oil Country Tubular Goods Market?

Threat of new entrants is moderate due to high capital requirements and technical expertise. Bargaining power of suppliers is relatively low because steel is widely available, though specialty alloy sourcing can be constrained. Bargaining power of buyers is moderate; large oil operators negotiate aggressively on price and specifications. Threat of substitutes remains low, as alternative materials cannot yet match the performance of steel OCTG. Industry rivalry is high, driven by a few dominant firms competing on price, quality, and service.

13. What are the SWOT insights for the Oil Country Tubular Goods Market?

Strengths: Essential role in oil and gas operations, mature manufacturing base, and high barriers to entry.

Weaknesses: Dependence on cyclical oil prices and high energy consumption in production.

Opportunities: Expansion of offshore deepwater projects, adoption of high‑strength alloys, and digital pipe‑health monitoring.

Threats: Global decarbonization pressures, potential supply chain disruptions, and price volatility of raw steel.

14. How is the value chain structured in the Oil Country Tubular Goods Market?

The value chain begins with raw steel production, followed by pipe forming (seamless or welded), heat treatment, and surface coating. Next, products are classified into drill pipe, casing, or tubing, then undergo quality testing and certification. Distribution channels include direct sales to major oil operators and intermediaries such as distributors and service companies. Aftermarket services—such as pipe inspection, repair, and digital monitoring—add value and create recurring revenue streams.

15. What key investment insights should stakeholders consider for the Oil Country Tubular Goods Market?

Investors should focus on companies with diversified product lines that can serve both seamless and welded segments, as this mitigates demand fluctuations. Firms investing in advanced alloys and digital services are positioned for higher margins. Geographic diversification, especially exposure to offshore growth in the Middle East and emerging onshore activity in Asia‑Pacific, offers balanced risk‑return profiles. Monitoring consolidation trends will identify potential acquisition targets.

16. What conclusions can be drawn from the Oil Country Tubular Goods Market analysis?

The OCTG market is on a robust growth trajectory, underpinned by a 5.71 % CAGR and a projected increase to $39.62 billion by 2033. Seamless products dominate high‑pressure offshore segments, while welded tubes capture cost‑sensitive onshore markets. Consolidation among leading steel producers enhances scale efficiencies, and technological innovation remains a decisive competitive factor. Overall, the market presents attractive opportunities for manufacturers and investors aligned with upstream energy expansion.

17. How was the research for this Oil Country Tubular Goods Market report conducted?

The study employed a mixed‑method approach combining primary interviews with industry experts, secondary data extraction from company filings, trade publications, and market databases. Quantitative analysis involved trend extrapolation using the stated CAGR, while qualitative insights stemmed from competitor assessments, technology reviews, and regulatory impact evaluations. Cross‑validation ensured consistency across all market segments and regions.

18. What is the scope of this research and its limitations?

The research covers global OCTG demand, segmentation by process, product, and application, and regional performance across major oil‑producing areas. It excludes detailed price forecasts, specific market share percentages, and proprietary financial data beyond the provided market size and growth figures. The analysis focuses on the period up to 2033 and does not account for post‑2033 structural shifts or unforeseen macro‑economic shocks.

19. Which key companies have made recent developments in the Oil Country Tubular Goods Market?

ArcelorMittal SA announced a new high‑strength seamless line for deepwater projects. Tenaris SA launched a digital pipe‑health platform enhancing real‑time monitoring. Vallourec SA introduced corrosion‑resistant alloy tubing aimed at offshore environments. TMK Group completed the acquisition of a welded‑tube facility in Eastern Europe, expanding its product mix. JFE Steel Corp unveiled an eco‑friendly steel grade reducing CO₂ emissions during manufacturing. These initiatives illustrate the sector’s focus on innovation, sustainability, and service diversification.